How PE-backed contractor consolidation is forcing rapid fleet standardization and early asset liquidation, creating an unusual supply of low-hour machines that sophisticated buyers are quietly absorbing.

Something Strange Is Happening in the Texas Used Equipment Market

Picture this: you are browsing used motor graders for sale in Texas, and right there between a 2009 Cat 140 Motor Grader For Sale with 9,200 hours and a worn-out Komatsu GD655 asking too much money, you spot a John Deere 872GP with 68 hours on the clock. Sixty-eight hours. This is a short-sighted pricing of used motor graders for sale in Texas between 9,200-hour 2009 Cat 140H costing sales and high asking prices of Komatsu GD655 with markedly worse mileage. That very grader sold for $660,000 at an August 2025 Lubbock auction, close enough to the price of ordering a new one.

Then you see another one. A Cat 150 with 370 hours, available at a sale in Humble, Texas. Half a dozen more motor graders under 1,500 hours were scattered across auction sites in the same quarter. None of these machines is worn out. None of them was sold because the owner had finished with the grading works. Something else is at play here altogether.

That ‘something else’ has a name: private equity-backed contractor consolidation. Once the mechanics behind this are understood, these listings stop looking random and become the inevitable output of a very deliberate financial playbook that cares nothing about the remaining service life of a machine and everything about standardizing a fleet before an exit.

Texas is the center for this story for discussed reasons, but the trend is changing the used motor grader market in the Gulf Coast and in other places. This article is going to change how you look at every near-new listing you see from now on if you buy, sell, or deal in heavy equipment, and you have not connected these dots yet.

The PE Roll-Up Wave Reaches Heavy Civil Construction

Private equity firms prefer fragmented industries. That, according to Wall Street, is a ‘roll-up opportunity,’ with hundreds of small, regional contractors doing $5M to $50M in annual take, each owned by someone with an eye on retirement, and operating much more on relationship and reputation than on systems and data.

You buy a platform company, bolt on regional players, create a national or super-regional footprint, squeeze out operational efficiencies, and sell the whole thing at a higher earnings multiple than any one piece would command.

That playbook was run on HVAC companies in the 2010s, pest control companies before that, and landscaping companies more recently. By the early 2020s, heavy civil construction, earthmoving, grading, road building, and underground utilities were in the crosshairs.

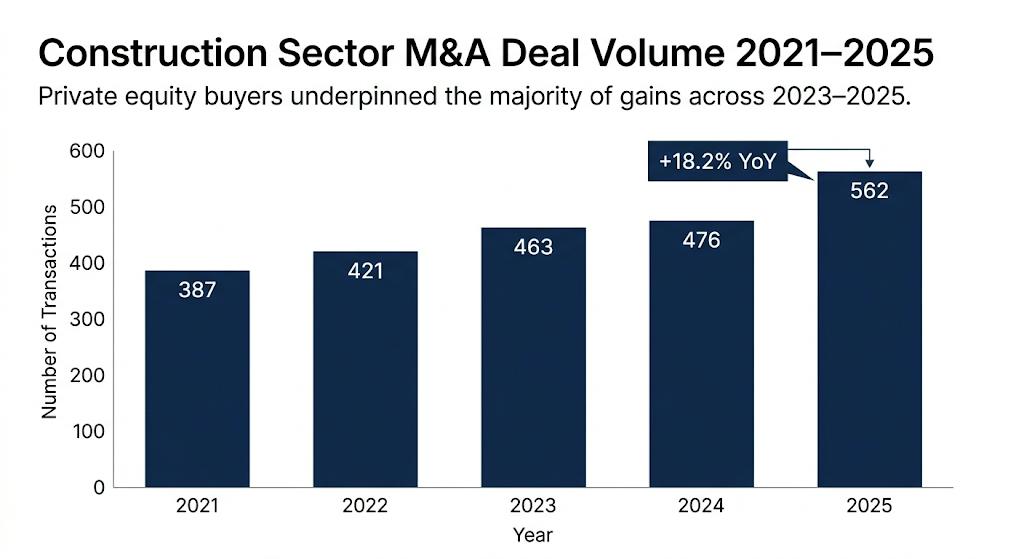

The numbers are evidence of this. Construction M&A activity expanded for the third consecutive year in 2025, with deal volume in the Construction Services sector reaching 562 transactions, an 18.2% increase over 2024. PE buyers accounted for a disproportionately high percentage of those transactions, attracted by IIJA-backed infrastructure demand, relatively guaranteed cash flows from contracts with state departments of transportation, and a fragmented competitive landscape still conducive to consolidation.

The common operational pattern starts when a private equity company discovers a successful contractor based in Texas, which operates a grading and site preparation business that generates 30 million dollars annually. The company will acquire five to eight small businesses that operate in nearby markets during the upcoming two to three years. Every acquired business will bring its own machinery, its dedicated brand partners, its trained personnel, and its specific operational procedures. The platform company now operates with 12 different shop foremen and various equipment from Komatsu, Volvo Cat, John Deere, Case, and AGCO, and its CFO needs to understand 14 maintenance systems.

Contact with the PE operations team destroys the present situation. The equipment story begins at this point.

The hold period matters enormously here. Most PE firms plan to sell within 4 to 7 years of acquisition, with some targeting faster exits if scaling conditions are right. The company makes all operational choices during this period to prepare for an impending sale.

The Integration Playbook: Fleet Standardization as Operational Mandate

The day after a PE-backed acquisition closes, a transition team typically descends on the acquired company. The first things they install are: unified financial reporting, a common ERP or accounting system, standardized safety protocols, and KPI dashboards that allow the parent platform to see every job, every margin, and every asset across the entire portfolio in real time.

The process requires essential equipment as its primary component. The method provides organizations with their most effective solution to achieve cost savings while maintaining operational efficiency. Fleet standardization exists as a mandatory requirement for all organizations that have completed their post-acquisition processes.

The operational case for standardization:

Parts commonality: If every motor grader in the fleet runs Cat 140-series components, you carry one parts inventory, not six. That alone can cut parts holding costs by 30–40%.

Technician training: Your mechanics become experts in one powertrain, one hydraulic system, and one telematics platform through their training. Your company eliminates overtime expenses because employees lack the necessary expertise to repair the Volvo.

Warranty and service programs: Cat Financial, Komatsu Care, and Deere’s PowerGard programs offer fleet pricing, but only if you’re running their iron exclusively. Mixed fleets forfeit this leverage.

Telematics integration: The modern fleet management platforms of Cat VisionLink and Komatsu’s Smart Construction ecosystem face compatibility issues when used with competitors’ equipment. PE-backed platforms use present-day asset utilization information to support their decisions about asset disposal and capital expenditure distribution.

The financial case for standardization: A standardized fleet shows better results for exit due diligence than operational benefits. The potential acquirer, who is either a strategic buyer or the next PE firm taking the company off your hands, does not want to inherit your mixed-brand fleet. Customers require Cat 140s to be stored at their yard with identical specifications, complete telematics records, and inclusion in the equipment maintenance system. The fleet functions as a financial resource. The mixed-brand equipment, which came from an acquired Beaumont, Texas contractor, represents an operational risk.

The main story element emerges because private equity-backed construction companies will sell machines that function well but are from an incorrect brand.

The Cat-standardized platform will discard a newly acquired 2022 1,200-hour Komatsu GD655 motor grader, which a family-owned contractor purchased brand new because of its acquisition by the platform. The machine operates without problems. The equipment has approximately 90% of its useful lifespan remaining. The equipment gets sold as a result.

Why Equipment Gets Sold Early: The Low-Hour Paradox

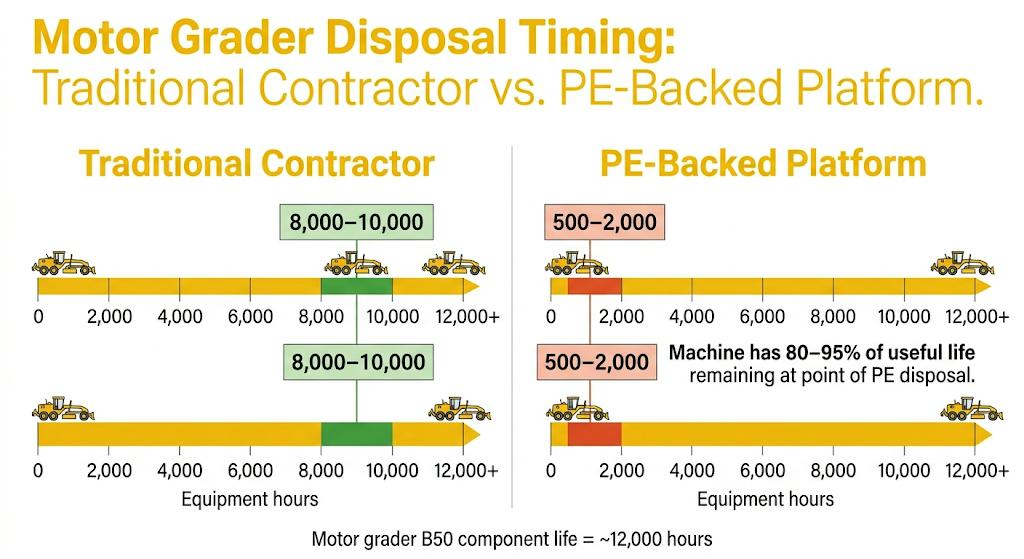

Traditional contractors keep their motor graders for extended periods. A family-owned earthmoving company might acquire equipment that they will use until it reaches both high usage and expensive repairs. Motor graders have an extended operational lifespan through their B50 component life, which lasts about 12,000 hours, because 20% of motor graders remain operational after 20,000 hours with standard maintenance.

The traditional ownership model establishes equipment disposal decisions according to the machine condition. Private equity owners base their decisions about equipment disposal on their corporate strategy.

The financial structure of a leveraged buyout creates upward momentum for this operational mechanism. The debt exists as part of the platform company’s financial obligation because private equity firms use debt to fund their acquisition of the platform. The debt agreement establishes interest payments along with a timetable for repayment and specific operational restrictions. The quickest method to enhance debt service coverage ratios requires organizations to transform their unused or inappropriate resources into liquid assets.

The acquired companies’ non-standard equipment serves as the business’s essential asset. A 1,500-hour grader that remains operational will generate cash through its sale at high market rates.

How PE platforms extract capital from fleet rationalization:

| Method | Mechanism | Typical Timeline Post-Acquisition |

| Outright Auction Sale | Fleet assets are sold through high-volume auctioneers like Ritchie Bros., IronPlanet, or Purple Wave. | 6–18 months post-close |

| Private Treaty Dealer Sale | Direct sale to a regional dealer to capture higher margins before resorting to a public auction. | 3–12 months post-close |

| Sale-Leaseback | Assets are sold to a finance company and leased back to the platform, freeing up immediate cash while standardizing the fleet. | 0–6 months post-close |

| Fleet Dispersal at Exit | A bulk liquidation of aging or non-core assets is conducted shortly before the PE firm sells the entire platform. | 12–24 months before exit |

Understanding the sale-leaseback process stands out as an important aspect to study. A construction company that receives private equity funding can transfer its complete equipment inventory to a third-party financing organization, which will provide instant cash to help cover acquisition debt while the company maintains operational control of the equipment through leasing arrangements. The company sells the non-standard equipment after the leaseback period ends because it remains in usable condition with minimal usage.

The planning process for exit-readiness serves as a third accelerator for business growth. Private equity firms establish their exit preparation processes about 12 to 18 months before they plan to sell their assets. The exit readiness checklist requires all organizations to conduct fleet rationalization. The upcoming 12 to 24-month period will result in equipment sales because private equity platforms need to sell their assets before they transfer ownership.

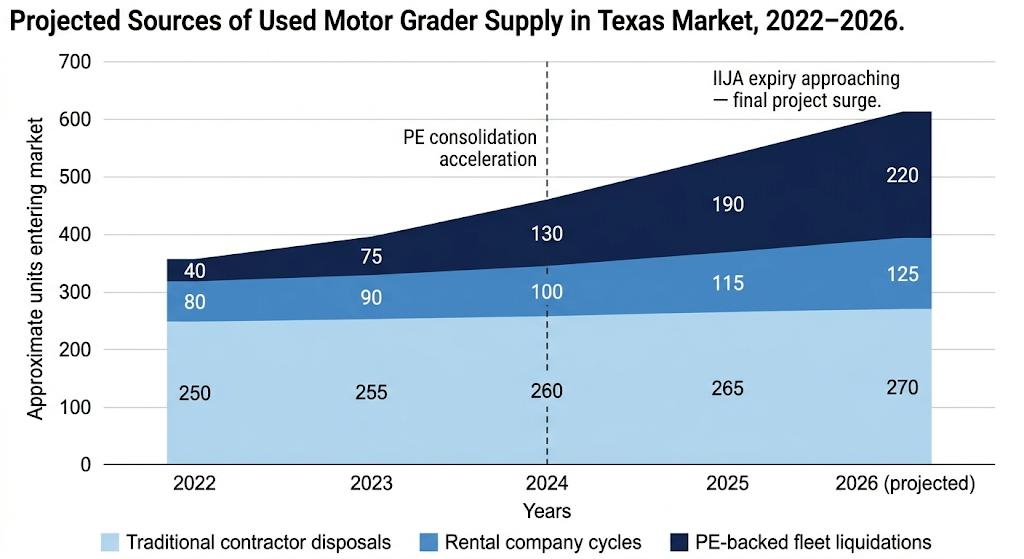

Texas as Ground Zero: Why the Gulf Region Is the Epicenter

The state of Texas serves as the main location that shows motor grader market results through PE-driven fleet liquidation. Texas serves as both a major construction market and its position as the highest motor grader purchaser in the United States.

Texas buyers purchased 319 used motor graders during the 12 months from November 2023 to October 2024, which represents the highest purchase total in the United States. The most recent comparable period showed 249 used units financed in Texas alone.

Top 5 States for Used Motor Grader Purchases (Units Financed, 2024–2025)

| Rank | State | Used Units Financed (2024) | Used Units Financed (2025) | YoY Change |

| 1 | Texas | 319 | 249 | -21.9% |

| 2 | California | 187 | 162 | -13.4% |

| 3 | Florida | 143 | 131 | -8.4% |

| 4 | Georgia | 118 | 109 | -7.6% |

| 5 | Colorado | 97 | 88 | -9.3% |

Source: Equipment financing data, 2024–2025 motor grader transactions. Texas consistently leads all states in both new and used motor grader purchases.

Why does Texas dominate? Several compounding factors:

- IIJA infrastructure spending: Texas received a major Infrastructure Investment and Jobs Act highway and bridge funding distribution for IIJA infrastructure spending. The high construction activity in Dallas-Fort Worth and the I-35 corridor and Gulf Coast port expansion projects has created ongoing demand for grading equipment, which will continue through 2025 and into 2026.

- Geographic scale of road work: Texas maintains the largest public roadway system in the United States, with more than 313000 lane miles of public roadway. The state needs more motor graders to maintain and extend its roadway system than any other state will ever possess.

- PE activity concentration: Private equity activity focuses on the Gulf Coast and Sun Belt corridor, which includes Texas, Louisiana, Georgia, and Florida, as these areas have become popular for private equity-backed contractor roll-up operations, which follow IIJA spending patterns.

- Port and industrial expansion: The development of the Houston Ship Channel and Corpus Christi port expansion and construction of LNG export facilities along the Gulf Coast has created site development projects worth billions of dollars, which require motor graders for site preparation.

The market exists because private equity companies supply low hrs motor graders for sale, while IIJA creates demand for operational graders, which results in an uncommon equipment market behavior that has appeared during recent times.

The Rental Amplifier: A Second Layer of Early Disposal

Low-hrs motor grader for sale, market dominance does not depend only on PE-backed construction contractors. Running a parallel playbook, many of which are backed by PE, rental firms provide an extra degree of near-new supply.

Valued at $151.61 billion in 2025, the worldwide market for building equipment rental is expanding swiftly. To keep equipment age competitive and reduce maintenance expenses, the major rental companies cycle their fleets aggressively. Regardless of hours, their target hold period for specialized equipment, including motor graders, is usually three to five years.

Though it is being cycled out to make room for a machine with the most recent emissions tier, most recent grade control technology, and telematics integration needed by the rental company’s platform, a motor grader acquired by a rental firm in 2021 might have 2,000 to 3,500 hours on it by 2025, a portion of its useful life.

Equipment Disposal Timeline Comparison: Traditional Contractor vs. Rental Company vs. PE-Backed Platform

| Owner Type | Typical Disposal Trigger | Average Hours at Disposal | Hold Period |

| Traditional Contractor | Rising repair costs or poor mechanical condition | 7,000–12,000 hrs | 8–15 years |

| Rental Company | Age or technological refresh cycles | 2,000–4,500 hrs | 3–5 years |

| PE-Backed Contractor Platform | Brand standardization or preparation for platform exit | 500–2,500 hrs | 12–36 months post-acq. |

| PE-Backed Rental Operator | Fleet consolidation following M&A activity | 800–3,000 hrs | 18–36 months post-acq. |

Combined effect: Multiple institutional ownership types are simultaneously disposing of equipment far below its operational life expectancy, concentrating supply in the used market.

The same fleet standardization reasoning applies when a PE business purchases a local rental company in Texas and combines it with its current rental platform. Non-conforming equipment from the bought rental fleet, running flawlessly, with low hours, is liquidated. The rental industry is both a parallel enhancer of the impact PE consolidation has on the market for used equipment and a contributor to the PE consolidation story.

The Market Pricing Reality: Discount or Premium?

Every purchaser wants to know: are these near-new, PE-liquidated motor graders selling at a discount, or do they hold value?

The response is complex and mostly dependent on who’s buying and where the device is marketed.

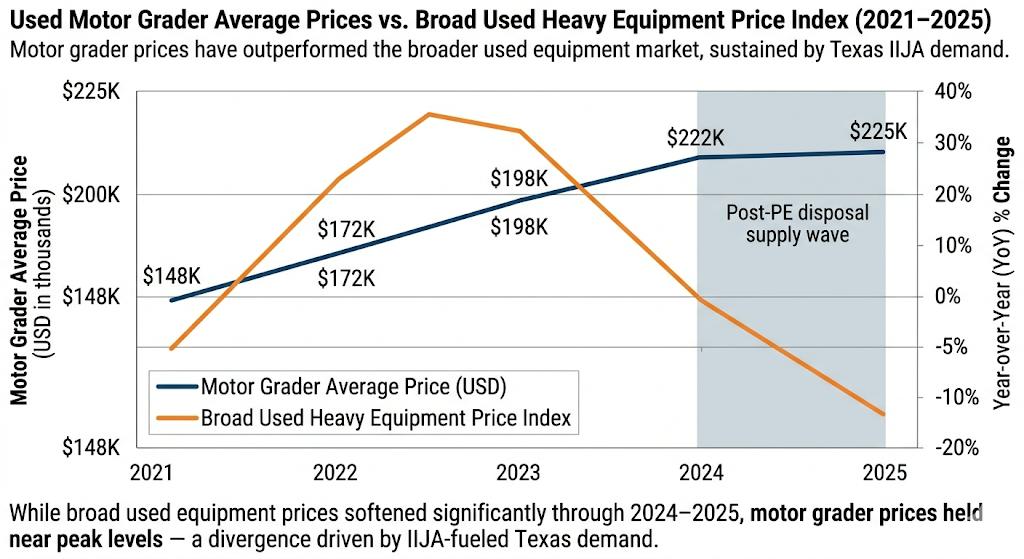

At the macro level, the values of utilized heavy equipment have decreased. U.S. used equipment resale prices were down roughly 7.27% year-on-year in Q3 2025; auction prices decreased as much as 17.13% year-on-year in certain sectors. As post-pandemic supply chain adjustments met demand, dealers were negotiating excess stock for much of 2024 and into 2025.

But low-hour used motor graders for sale in Texas have acted apart from the general market.

Used Motor Grader Pricing Summary (2024–2025)

| Metric | Value |

| Average used motor grader price (Jan 2025 peak) | $230,146 |

| Average used motor grader price (Sept 2025) | $221,312 |

| Price change, Jan–Sept 2025 | -3.9% |

| Average age of used motor grader on the market | ~9.5 years |

| Auction record (John Deere 872GP, 68 hrs, Lubbock, TX, Aug 2025) | $660,000 |

| Near-new Cat 150 (370 hrs, Humble, TX, 2024) | ~$520,000 |

| Overall, used heavy equipment price change in Q3 2025 YoY | -7.27% |

The main realization is that motor graders have decreased much less than the general market for used goods. Why not? Particularly for late-model, low-hour, provable functioning machines, Texas demand, driven by IIJA highway and bridge expenditures, has established a pricing floor.

Just because it has a few hours, a near-new machine from a PE-backed fleet liquidation does not sell at a great discount. Actually, it sometimes commands a premium above the market average just because consumers can see the maintenance records, confirm low utilization, and trust the condition. The extent of any discount results from the supply volume. Competition between vendors can push prices a little lower than their respective possible when several low-hour graders show up in the same auction cycle or under listings for the same area at once. These systems, however, are not worn-out assets. These pieces of equipment, being sold for structural reasons unrelated to the machine itself, are clean and well-kept.

The Invisible Buyer Chain: How Sophisticated Players Absorb Before Retail

This is the segment of the narrative most solo purchasers never see, since the best machines are already gone when they start looking over listings.

Buyers who move at various speeds and have varied access to knowledge have a very genuine hierarchy. In a matter of days or weeks, not months, near-new equipment from PE-backed fleet liquidations goes via this chain.

The Buyer Hierarchy for PE-Liquidated Motor Graders:

Tier 1 – Worldwide Exporters: Days 1–15 International equipment exporters aiming for the Middle East, Southeast Asia (Vietnam, Indonesia, Philippines), and West Africa are the fastest and most aggressive customers in this market. At PE-backed systems, these customers build relationships with fleet managers and auction houses; they pledge to equipment before it appears on public listings. A 1,200-hour Cat 140M motor grader destined for Saudi Arabia or a road construction project in Nigeria is contesting with a buyer in Dubai who already knows the machine exists and has a shipping container ready, rather than with your local contractor buddy. With customers in over 190 nations, auction companies like Ritchie Bros. frequently set a lower limit for pricing for low-hour, late-model equipment.

Tier 2: Regional Dealers, Days 5–30, Cat dealers, Komatsu dealers, and independent used equipment retailers, established Texas-based heavy equipment dealers, keep continuous contact with fleet managers at PE-backed platforms. They get calls before machines appear at public auction. In return for a little discount from auction value, a seller can provide speed and clarity. The machine lists with a margin at retail, gets once-over, then enters inventory. Somebody has already profited on it by the time it shows up as a retail listing on MachineryTrader or IronPlanet.

Tier 3: Large Fleet Operators (Days 15–60) Businesses managing vast, geographically dispersed activities, national road contractors, major mining corporations, state DOT contractors, track bulk fleet sale alerts, and keep procurement relationships with PE-backed platform companies. Attractive customers for a PE platform attempting to get rid of a mixed fleet in one transaction, they can ingest three or four machines on one purchase order.

Tier 4: Individual Contractors and Small Fleets, Days 30–120+. The Tier 1 and Tier 2 buyers have already made their choice by the time an individual contractor is searching used motor graders for sale in Texas listings on IronPlanet or browsing auction previews. What’s left are either machines that failed Tier 1 and Tier 2 criteria, or machines that required more hours, less appealing specs, pricing above what exporters would commit to, or machines that fell through the network and arrived at public auction by default.

The time difference here is intentional. It is the structural outcome of information inequality. Daily market participants, exporters, and dealers know before anyone else when a PE-backed platform is reducing its fleet. Individual contractors learn the listing’s timing.

What Sophisticated Buyers Know & How to Position Yourself

Only if you can act on it is knowing the PE-driven fleet liquidation mechanisms beneficial. Buyers who successfully buy low-hour machines from these events actually perform differently here:

- Look at the M&A timeline, not just the auction calendar. Place a 60–120-day marker in your calendar whenever a PE company declares the purchase of a Texas or Gulf Coast construction contractor. Usually, following inside that window as integration teams evaluate equipment overlap, are fleet rationalization choices. First access is available by means of a quick call to the equipment manager of the purchased company, who sometimes knows exactly what’s going to be dumped before the PE platform has formally recorded anything.

- Understand the distinction between individual listings and fleet dispersal sales. An event called a fleet dispersal sale, where a PE platform auctions 20 to 40 pieces of equipment from many acquired firms, is quite a different beast from an individual machine listing. Because the vendor is moving volume, fleet dispersal sales sometimes comprise the best machines and can provide pricing benefits when several buyers are targeting different devices and not all competing on the same grader.

- Develop Texas vendor relationships rather than only internet search trends. Your best advance notice on low-hour PE-liquidated equipment comes from the Tier 2 dealer network. PE platform firms frequently contact Houston, Dallas, and San Antonio cat dealers before auctions. Should a dealer be aware that you’re a serious buyer for a particular motor grader specification, they will phone you before they list it.

- Examine telematics records rather than just hour counters. Platforms supported by PE conduct telematics on everything. Ask for the telematics download when assessing a nearly new motor grader from a fleet liquidation; it will reveal actual usage patterns, inactive time levels, geographic distribution, and any registered fault codes. Often more revealing than the visual examination, this information will be readily available to vendors with nothing to conceal.

- The time window closes fast. From the time a PE platform makes a fleet rationalization choice until Tier 1 and Tier 2 consumers take in the finest machines is sometimes only 30 to 90 days. You are always arriving after the best inventory is committed if you are waiting passively for computers to show in retail listings.

What This Means for the Used Grader Market Through 2026 and Beyond

Over the following 12 to 24 months, many factors are converging on the used motor grader industry; knowing these can significantly affect purchasing and selling choices.

The dynamics of the expiration of the IIJA: In September 2026, most of the highway and bridge funds in the Infrastructure Investment and Jobs Act will likely run out. Knowing this, state DOTs and contractors are giving awards and mobilising the last burst of IIJA-funded projects right now through 2025 and into early 2026. This is when motor graders reached their greatest demand. Those who buy machines in 2025 for IIJA work will be in a good position; those who wait till after the expiry may find both the work and the equipment demand softening simultaneously.

The PE departure wave: Construction M&A reveals no indications of decelerating. As hundreds of PE-backed construction platforms are 3 to 6 years into their holding periods, exit waves are growing. Platforms purchased in 2019–2021 are arriving at or nearly their normal exit windows. Every exit produces a new fleet rationalization, either by the selling PE company in the 12–18 months before exit or by the acquiring business after close, as they merge the acquired platform into their own uniform fleet. More PE roll-ups call for more brand standardizations.

Self-reinforcing cycle: Increased standardization demands more early removal of non-conforming gear. More early disposal results in more low-hour devices on the market. Unless PE construction spending slows significantly, this cycle has no natural brake, which current M&A data does not indicate.

The long-run market impact: The used motor grader sector is undergoing permanent re-adjustment. Over the last several years, used motor graders on the market have averaged about 9.5 years; nevertheless, as PE-backed fleet liquidations become a bigger part of supply, that average will lean younger. A market formerly sorting itself between new and used/worn is now growing a third category: institutionally cycled, low-hour, late-model, with recorded maintenance history, priced lower than new but higher than typical used. Over 2026 and beyond, this section will see the most fascinating price and value dynamics.

A Market Hiding in Plain Sight

The nearly new motor graders seen in Texas with equipment listings are neither an anomaly nor a coincidence. They are the downstream output of a financial system that works on its own logic, one that has nothing to do with equipment condition and everything to do with brand standardization, capital recycling, debt service, and exit preparation.

It makes no difference that the Komatsu GD655 from one of those acquisitions has 800 hours and runs like new when a PE business buys five local contractors in Texas and combines their fleets into one regular brand. It’s the wrong kind. Furthermore, Texas is the most active corridor for PE-backed construction consolidation and the biggest motor grader market in the nation; the impact is concentrated here in plainly evident ways, if you know what you’re seeing.

This is a planned opportunity for purchasers who grasp the fundamentals: access to machines with the great majority of their working life still intact, recorded maintenance history, and pricing motivated by institutional need instead of market weakness. For people who don’t, the window closes before they see, absorbed by exporters and dealers who do this every week.

The most costly machines on the used market sometimes provide the greatest discounts. Not despite the price, but rather since the purpose of their selling has nothing at all to do with the equipment.

FAQs

1. Why would a company supported by PE sell a motor grader that has only 500 hours on it?

A: Because brand standardization, not machine condition, drives fleet decisions under PE ownership. When the platform standardizes on Cat, a 500-hour Komatsu becomes surplus because it’s the wrong brand.

2. Are these low-hour PE-liquidated motor graders genuinely inexpensive, or are they flawed?

A: They are typically genuinely clean machines that were disposed of for portfolio rather than mechanical reasons. To confirm utilization history and make sure there are no recorded fault codes, always ask for the telematics download.

3. How can independent contractors compete with first-access dealers and exporters?

A: Within 60 to 90 days of closing, keep an eye out for M&A announcements and give the fleet manager of the acquired company a call. This is before the majority of machines go public. Before the auction, dealerships in Houston, Dallas, and San Antonio will also reveal machines.

4. Is this trend of almost-new used motor graders going to last, or is it just a fad?

A: It is not transient, but structural. Early fleet disposals will continue to fuel the used market as long as PE firms continue to buy, combine, and sell construction platforms, and the current M&A pace shows no signs of slowing.