You can hear a variant of this story that is almost too abstract to worry about: Oil futures, Strait of Hormuz closures, geopolitical risk premiums. De-jargon it all, and you have something very tangible: a contractor in Texas attempting to make up his mind whether to purchase a used grader this quarter is now doing so in a world redefined by airstrikes and naval blockades and a global energy shock that already has economists comparing it to the crises of 1973 and 1979.

The US-Israel-Iran war, which started on February 28, 2026, with synchronized American and Israeli attacks on Iranian military installations, has caused shockwaves in the commodity markets, the construction supply chain, and equipment financing terms that extend all the way to the auction lanes and dealer lots where the used motor grader market in the US conducts its daily business. This is not a theory. It is currently occurring, and anyone who sells, buys, or operates a motor grader in America must know precisely what forces are at work.

This paper is a comprehensive record of those forces: where the battle is, what it has done to the inputs on which construction relies, how it is changing contractors’ behavior, and what the overall impact is on the purchasers and sellers of used motor graders in the USA.

The War That Changed Everything: A Brief Contextual Reset

You must first of all understand the magnitude of what actually occurred to comprehend the market effects. It was not a one-time airstrike or a short-term engagement. On 28 February 2026, the United States and Israel undertook a very well-planned air attack on Iranian military installations and the highest leadership of the Islamic Republic, assassinating the Supreme Leader Ayatollah Ali Khamenei. Iran retaliated by firing missiles and drone attacks on US military bases, Israeli targets, and energy infrastructure in the Gulf states, involving at least 14 other countries in the Middle East and beyond in the conflict.

The war soon became what world economists term a structural shock to the global economy. The World Economic Forum termed the domino effect as radiating far beyond the Gulf, restructuring global commodity markets, food systems, industrial supply chains, financial situations, and geopolitical alignments, possibly over many years to come.

The most significant physical event was the sealing of the Strait of Hormuz on March 4, 2026, the shipping passageway through which about 20 percent of all oil and a fifth of all LNG in the world had passed. That chokepoint was effectively closed, and the energy markets were in historic territory. Brent crude surged past $120 per barrel. Gulf oil producers such as Kuwait, Iraq, Saudi Arabia, and the UAE reduced production by at least 10 million barrels per day. Brent crude is currently trading at around $102 per barrel, a 40 percent gain since the war broke out, and WTI, the US standard, is over 104, or more than 50 percent above the pre-war price.

The engine of that energy shock is the driving force of almost all the downstream impacts on the construction and heavy equipment industries, including the used motor grader market in the US.

Where the Used Grader Market Stood Before the Storm

Here, context is everything. The used motor grader market in the US was not in a strong position when the conflict erupted. It had already weakened for over a year, and the realization of that baseline tells you a lot about the way the geopolitical shock is interplaying with underlying conditions.

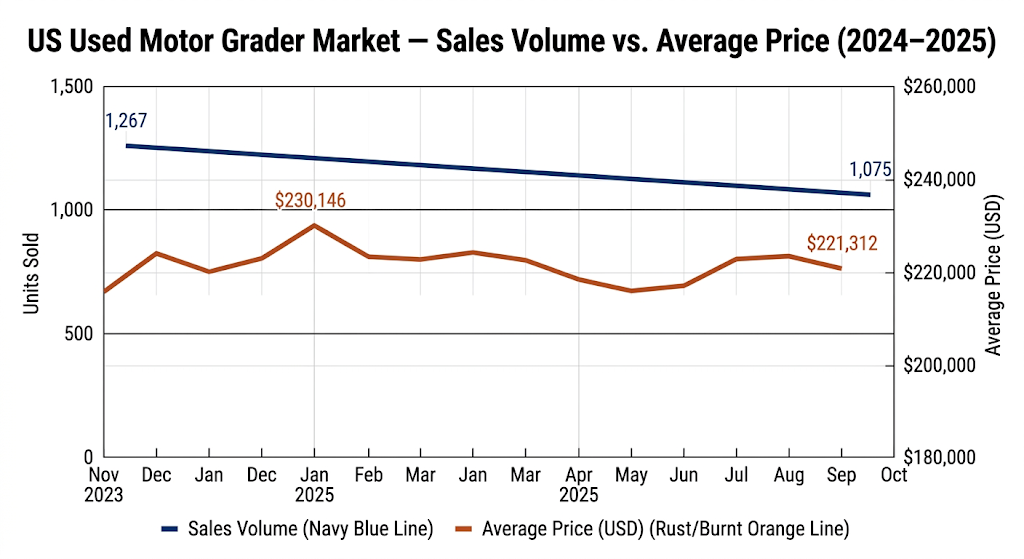

The EquipmentWatch data of Fusable shows that the average price of a used motor grader will reach its highest point of $230,146 in January 2025, and then drop to 221,312 by September 2025, a slight correction of about 3.8%. More significant was the volume picture: the used motor grader sales were 1,075 units in the twelve months ending October 2025, a decrease of 15.2% compared to 1,267 units in the previous year period. The number of new motor grader sales also decreased by 6.7 percent during the same window, with 808 units being sold on finance. The average age of motor graders that were on sale remained at about 9.5 years during this time.

Used motor grader sales volume and average price trend, January 2024 to October 2025.

Caterpillar controlled both markets, with 60.8 percent of all new financed motor graders and 47.3 percent of all used financed models sold. John Deere was second, and Komatsu was third. CAT sold 243 more new units than its closest competitor over the period.

The market, briefly, was undergoing a slow-motion correction: healthy prices but falling volumes, but then the geopolitical shock came and presented a whole new set of variables.

US Used Motor Grader Market | Key Baseline Metrics (2024–2025)

| Metric | Value |

| Average used motor grader price (Jan 2025) | $230,146 |

| Average used motor grader price (Sep 2025) | $221,312 |

| Used motor grader units sold (Nov 2024–Oct 2025) | 1,075 units |

| Year-over-year decline in used sales volume | –15.2% |

| New motor grader units sold (same period) | 808 units |

| Year-over-year decline in new sales | –6.7% |

| Average age of used graders in listings | ~9.5 years |

| Cat market share, new financed units | 60.8% |

| Cat market share, used financed units | 47.3% |

| Secondary market annual growth (compact graders) | 8% |

The Diesel Shock: Fuel Costs and Grader Economics

One of the most fuel-consuming machines on any job site is the motor grader. An average mid-size grader that works eight-hour shifts burns a significant amount of diesel per working day, and when the cost of this fuel doubles in just a few weeks, the calculations on all grading contracts in America are altered.

The average US regular gasoline was at 2.98 per gallon before the start of the war. By mid-March 2026, this number had already reached $3.58, an increase of 20 percent, and analysts at Gulf Oil are telling them that wholesale gasoline futures may continue to go up. Diesel, which fetches a higher price than regular gasoline and follows the crude oil prices even more closely, has seen a correspondingly greater increase. Reports indicate that with oil prices exceeding $110 per barrel at the peak of the conflict, the spike in oil prices would be a major contributor to the US inflation rate, with some professionals saying that the longer the spike lasts, the greater the shock would be.

This dynamic of fuel works both ways to the operators sourcing Used Motor Graders For Sale In USA. It adds to the cost of operating whatever equipment they already have, and this constrains project margins and causes contractors to hesitate to add to their fleets. Meanwhile, increased fuel prices elevate the fuel efficiency of a prospective used grader acquisition to a greater assessment factor than it was half a year ago. The buyers considering Used Motor Graders For Sale In USA in 2026 are examining the fuel consumption information much more closely than their peers in 2022 or 2023.

Steel, Aluminum, and the Parts Problem

The second significant avenue of the conflict in the construction and equipment industry is the route of raw materials. The metals from which motor graders are constructed and repaired.

The closure of the Strait of Hormuz did not affect oil tankers alone. It interfered with an incredibly wide spectrum of industrial feeds that pass through the Gulf. The most acute case is that of aluminum. The Middle East has become the largest producer of over 8 percent of the total world production of aluminum, with the Gulf Cooperation Council countries increasing their output to above 6 million tons as compared to less than 3 million tons in 2010. Two of the largest aluminum manufacturers in the region, Qatar and Bahrain, have already halted shipments to international clients, compelling US manufacturers and equipment companies to find other sources in Asia and Australia.

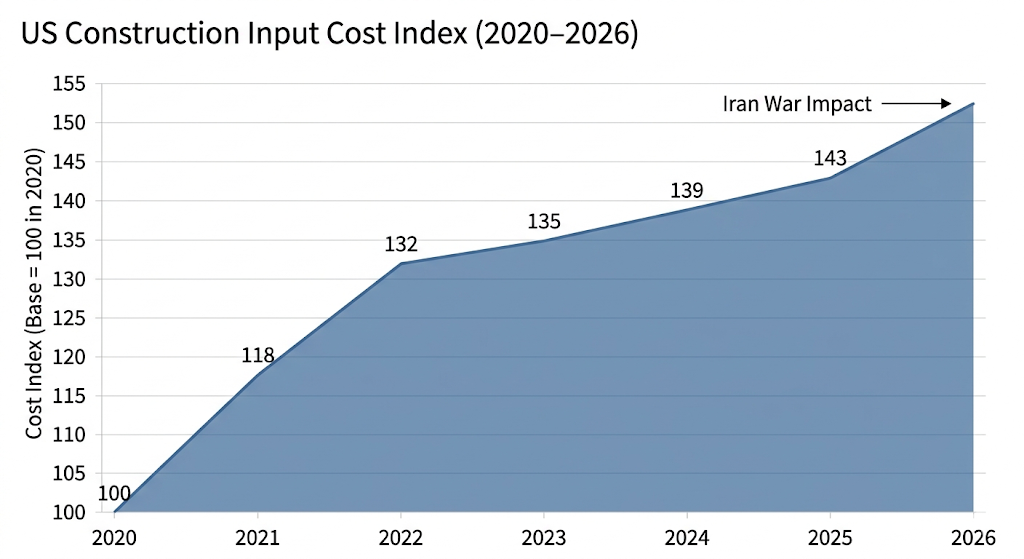

The cost of construction inputs had already increased by over 40 percent since early 2020, and US builders and equipment manufacturers were already grappling with these increased costs. By early 2026, the Associated General Contractors of America had estimated an additional 6.2% per annum rise in construction input costs, pushed by the soaring prices of aluminum, steel, and copper, which are the very materials used to make grader frames, blades, hydraulic systems, and parts of the drivetrain.

Construction input cost index (2020–2026), showing the cumulative 40%+ rise and the 2026 conflict-driven acceleration.

The sulfur disruption is a less-reported but critically important subplot. The Gulf region contributes about 45 percent of all sulfur in the world, and sulfur is needed in the manufacture of sulfuric acid, which is a major raw material in the processing of copper ore. Reduction of sulfur availability translates to reduction of copper availability, which is directly channeled to the electrical systems, wiring, and precision components utilized in the contemporary motor graders. The Institute for Supply Management cautioned that supply chains that undergo disruption record an average increase of 40% in cost-to-serve post-disruption, which includes precisely such cascading material constraints.

Key Raw Materials Affected by the Conflict &Their Grader Market Relevance

| Material | Primary Disruption | Middle East Supply Share | Grader Component Impact |

| Crude oil/diesel | Strait of Hormuz closure | ~20% of global oil trade | Direct operating cost increase |

| Aluminum | Qatar & Bahrain suspended deliveries | ~8% of global production | Cab structures, hydraulic parts |

| Steel | Energy cost pass-through; logistics | Regional supply contribution | Blade, moldboard, frame components |

| Copper | Sulfur shortage → reduced processing | Indirect (sulfur: ~45% global) | Wiring, electrical systems, sensors |

| Sulfur | Gulf GCC production halted | ~45% of global supply | Copper processing input |

| LNG / natural gas | Strait closure, QatarEnergy force majeure | ~20% of global LNG trade | Manufacturing energy cost |

New Equipment Supply Chains Break Down & Buyers Turn to Used

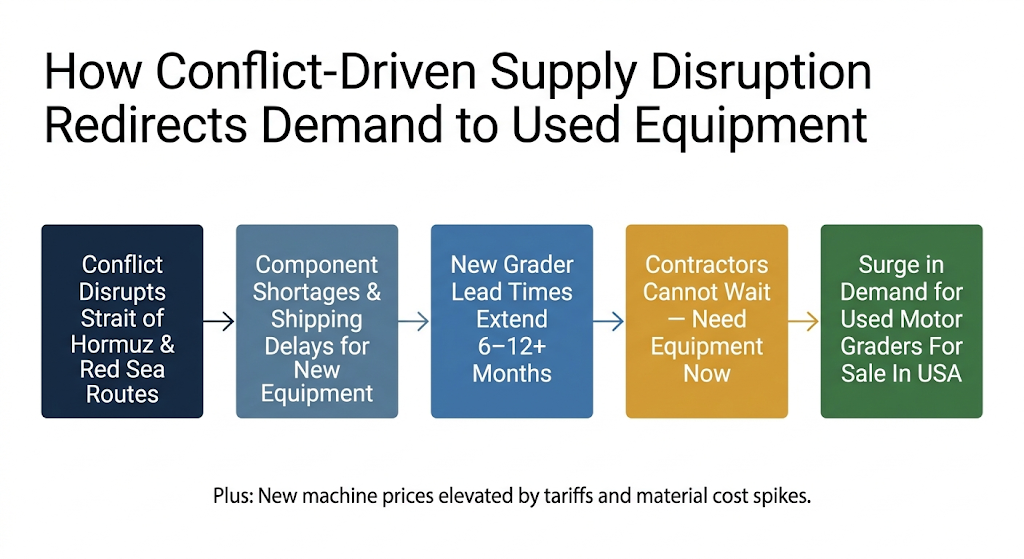

This is the part of the story that the used motor grader market US actually benefits from, and it is worth understanding precisely why.

When new equipment supply chains get disrupted, whether through component shortages, shipping delays, or manufacturer production constraints, buyers who need a machine now cannot wait six, eight, or twelve months for a new order to arrive. They turn to the used market. This “flight to available inventory” effect is one of the most consistent dynamics in the heavy equipment industry during periods of supply chain stress, and the 2026 Iran conflict is generating exactly these conditions.

Analysts at Xeneta, the global freight intelligence platform, stated that the repercussions of the US-Israel military operation against Iran will result in “further weaponization of trade” and will “shatter hopes of a large-scale return of container shipping to the Red Sea in 2026.” Many carriers had already been sailing around the Cape of Good Hope, adding weeks to delivery schedules, due to attacks by Iran-backed Houthi militias in the Red Sea. The new conflict has indefinitely extended that rerouting reality.

Motor graders from Caterpillar, Komatsu, John Deere, and Volvo all rely on globally sourced components. Extended lead times on new machine orders, already stretched by the prior Red Sea disruptions, are now being stretched further by the broader Middle East conflict. A contractor who would previously have ordered a new Cat 140 and waited four months for delivery now faces an uncertain wait of potentially six months or more, with no firm pricing guarantee given raw material volatility.

The result: more contractors are searching for Used Motor Graders For Sale In USA right now than they were a year ago. Online search activity for used grader inventory is increasing, and well-maintained units with documented service histories are clearing auction lanes quickly. As one market analysis published in early 2026 noted, “units that have well-documented services attract high bids,” and “mid-range graders in good condition are auctioning fast.

The supply chain disruption cycle: how conflict-driven new equipment delays drive demand toward the used motor grader market.

Construction Spending Pulls Back: The Demand-Side Headwind

Not all of the conflict’s effects on the used motor grader market in the US are supportive. Construction spending itself, the activity that motor graders exist to serve, is contracting, and that contraction represents a genuine headwind to grader demand.

US construction spending slipped in January 2026, with private construction spending falling 0.6% and residential construction dropping 0.8%. Construction payrolls declined by 11,000 jobs in February 2026, prompting the Associated General Contractors to note that “contractors may be more reluctant to add workers amid uncertainty about how much they will pay for construction materials and demand for certain types of construction projects.”

The housing market is a particularly significant bellwether. Construction experts have noted that the US housing market entered 2026 already in a severe affordability crisis, with a shortfall estimated between 2 million and 20 million units, depending on methodology. The Iran war is now throwing “another spanner in the works,” as one Newsweek analysis put it, with oil and gas prices soaring and construction material costs threatening to make the affordability gap worse, not better. With builders already trimming home sizes, redesigning layouts, and offering sales incentives on 64% of new homes to keep buyers engaged, the appetite for fleet expansion among residential contractors is understandably muted.

The Tariff Multiplier: A Pre-Existing Wound Made Worse

The conflict did not arrive in a clean policy environment. The Trump administration’s sweeping tariff policies, particularly tariffs on steel, aluminum, and a broad range of imported manufactured goods, had already elevated the cost baseline for new equipment before a single missile was fired at Iran.

The cumulative effect of tariffs and conflict is what economists call a “double shock.” New graders are more expensive because of the tariff-driven cost increases embedded in their price tags, and now those same machines are further burdened by material cost spikes and supply chain uncertainty. For buyers already priced out of the new equipment market by tariff-inflated sticker prices, the conflict provides additional justification to look at Used Motor Graders For Sale In USA rather than committing to a new machine.

This dynamic is showing up in buyer behavior. Market data from 2024 through 2026 shows that contractors are increasingly focused on return on investment rather than brand popularity, and that large-volume buyers in particular are factoring in the total cost of ownership, including purchase price, fuel cost, maintenance cost, and resale value, rather than simply defaulting to the most recognized brand. In a tariff-and-conflict environment, a well-maintained used grader from a proven manufacturer can represent dramatically better value than a new machine with an inflated sticker price.

Financing Costs and the Market’s Quiet Squeeze

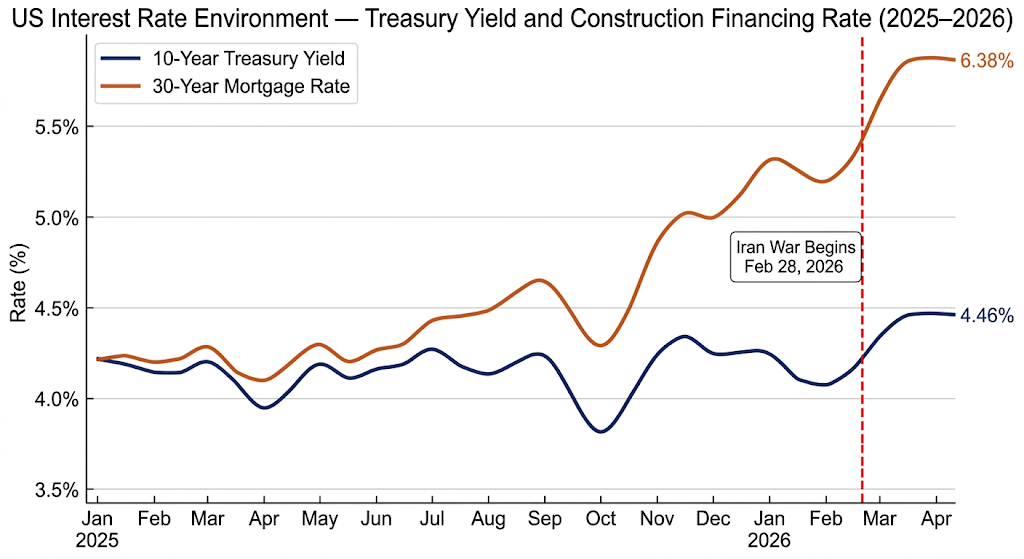

Equipment purchases are almost always financed, which means interest rates are a critical variable in any discussion of the used grader market. Here, the Iran conflict is creating additional pressure through its inflationary effects on the bond market.

On March 27, 2026, the 10-year Treasury yield jumped to 4.46%, its highest level since July 2025. The 30-year mortgage rate climbed to 6.38% on March 26. The Federal Reserve, which had been expected to continue cutting rates through 2026, is now facing a dilemma: the conflict-driven energy shock is pushing inflation upward even as the broader economy faces recession risk. The IMF has already warned that “if prolonged, higher energy prices will lead to higher headline inflation,” while the Dallas Fed’s research quantifies scenarios where Q4/Q4 inflation in 2026 could be materially higher than pre-conflict forecasts, depending on how long the Strait of Hormuz remains disrupted.

For equipment buyers, elevated interest rates mean higher monthly payments on equipment loans and finance leases. This can make even a reasonably priced used grader feel expensive when the financing terms are worked out. It creates a preference for leasing or renting over buying outright, a dynamic that suppresses used grader transaction volumes even while it supports rental rates and maintains demand for available inventory.

US 10-year Treasury yield and construction financing rate trajectory, 2025 to April 2026, showing the conflict-driven spike.

The Infrastructure Lifeline: Why the Floor Holds

Despite the pressure from multiple directions, the used motor grader market in the US is not collapsing, and the primary reason is federally funded infrastructure spending. Motor graders are, at their core, road-building and site-grading machines, and the US government spends over $100 billion annually on road maintenance and construction projects that require exactly this kind of equipment.

Federally funded projects operate on timelines and budgets set months or years in advance. A state transportation department that approved a highway resurfacing project in fiscal year 2025 is not going to cancel that project because oil prices spiked in March 2026. The contractors awarded those projects still need graders, still need to deploy equipment, and still need to acquire or maintain their fleets accordingly. This insulation from short-term energy shocks means that the infrastructure sector provides a durable floor under greater demand, particularly for the mid-size units that are the bread and butter of highway maintenance work.

The Infrastructure Investment and Jobs Act, whose funding continues to flow into state and local projects, provides an additional layer of demand stability. While private residential and commercial construction is pulling back, public infrastructure work is proceeding, and the Used Motor Graders For Sale In USA most relevant to this segment, proven, reliable units in the 120–170 horsepower range, are seeing consistent buyer interest.

Net Impact Assessment: Iran Conflict Effects on the US Used Grader Market

| Impact Channel | Direction | Mechanism | Intensity |

| Diesel/fuel prices | Negative for operators | Oil at $100+; 20%+ fuel cost increase | High |

| Steel and aluminum prices | Negative (maintenance costs) | Gulf supply disruption; shipping rerouted | High |

| New equipment supply delays | Positive for used demand | Buyers pivot to available used inventory | Medium–High |

| Construction spending slowdown | Negative (demand side) | Private construction falls; projects paused | Medium |

| Tariff-inflated new prices | Positive for used appeal | Used graders are relatively more affordable | Medium |

| Higher interest rates/financing | Negative (transaction volume) | Fed pressure; buyers prefer leasing | Medium |

| Federal infrastructure spending | Positive (demand floor) | Public contracts insulated from short-term shocks | Medium |

| Supply chain uncertainty | Mixed | Delays push some to used; uncertainty deters others | Mixed |

What Buyers and Sellers Should Actually Do With This Information

Understanding the macro picture is only useful if it translates into actionable market intelligence. Here is what the current environment actually implies for the two sides of the used grader transaction.

For buyers looking at Used Motor Graders For Sale In USA, the current environment rewards preparation and speed. Well-maintained units with documented service records are clearing faster than they did eighteen months ago, and price negotiation leverage has shifted modestly toward sellers in the quality segment of the market. The used motor grader market in the US is not a buyer’s market right now; it is a market of scarcity in the upper-quality tiers, where infrastructure contractors and municipal buyers are competing for the best units.

Buyers should also be thinking carefully about fuel efficiency specifications, given the elevated diesel environment. The difference between a grader consuming 4 gallons per hour versus 5.5 gallons per hour is a much larger annual operating cost differential at $5-per-gallon diesel than it was at $3.50 diesel. Volvo G946B units and Komatsu GD655-7 models have been noted in recent contractor surveys for fuel efficiency advantages in mixed-load conditions, and these performance characteristics are increasingly factored into purchase decisions.

Sellers, meanwhile, are in a relatively favorable position for quality inventory but should not mistake elevated demand for unlimited pricing power. The financing environment is working against buyers, and machines priced at the high end of the market will face resistance from buyers who are simultaneously dealing with higher operating costs, higher material costs, and more expensive financing. The sweet spot in the current used motor grader market in the US is a well-documented machine priced competitively, one that removes the buyer’s risk perception rather than maximizing the seller’s short-term return.

A Market Navigating Uncharted Crosswinds

What the US–Israel–Iran conflict has done to the used motor grader market US is not a single clean effect; it is a web of intersecting pressures that point in different directions simultaneously, requiring buyers, sellers, and fleet managers to think more carefully than usual about every decision.

The honest summary is this: the energy shock is real and consequential, raising the cost of operating every piece of diesel-powered equipment in America. The material cost surge is real and consequential, making repairs and new equipment alike more expensive. The supply chain disruption is real and, paradoxically, somewhat supportive of used market demand. Construction spending is softening in the private sector but holding up in the public infrastructure arena. And the financing environment is creating transaction friction that keeps overall market volumes compressed even when demand interest remains present.

The used motor grader market US in 2026 is what you might call a “thin but priced” market, one where transaction volumes are constrained but where good-quality machines are holding their value because the combination of new equipment uncertainty, tariff pressure, and supply chain disruption has elevated the functional attractiveness of well-maintained used iron. Anyone sourcing Used Motor Graders For Sale In USA today is operating in a more competitive environment for quality units than they were a year ago, and anyone selling quality inventory is finding a receptive audience, as long as the pricing reflects the realities of a market where buyers are also absorbing significantly higher costs on every other line item in their business.

The war in Iran may eventually de-escalate. The Strait of Hormuz may reopen. Oil prices may normalize. But the structural lessons of this period, about the importance of equipment availability, the cost of supply chain fragility, and the value of holding maintained, operational assets in a world where new supply can be cut off almost overnight, will shape the heavy equipment market in America for years to come.

FAQs

Q1: Are used motor grader prices expected to rise further because of the Iran conflict?

A: Prices for quality used units are likely to remain elevated as long as new equipment lead times stay extended and construction activity holds up through government infrastructure spending. Expect the middle tier to stay firm.

Q2: Should I buy or rent a grader given the current uncertainty?

A: Renting makes sense for short-term project needs given elevated financing costs, but for contractors with predictable, multi-year infrastructure workloads, purchasing Used Motor Graders For Sale In USA still provides better long-term economics than continued rental expense.

Q3: Which grader brands are holding their value best in the current market?

A: Caterpillar continues to dominate both sales and resale value, holding 47.3% of all used financed unit sales. John Deere and Komatsu follow, though Volvo and Komatsu units are increasingly favored for fuel efficiency in cost-sensitive environments.

Q4: How long is this geopolitical disruption likely to affect the used motor grader market US?

A: Based on analyst projections, oil price normalization requires the Strait of Hormuz to reopen and carrier confidence to return, a process estimated at two to three months minimum after active conflict subsides. Material cost relief will lag oil price recovery by several additional months.

Tags: Grader Market Analysis USA, Grader Market Insights, Motor Grader Market 2026